Scaling Threat Modeling for Banking Apps

Date

Authors

Tony UV

Follow Us

A practical guide for mid-sized financial institutions moving beyond manual threat modeling

For mid-sized financial institutions, threat modeling services for financial institutions are no longer a niche application security exercise. They are becoming essential as banking applications expand across mobile banking, digital onboarding, payment rails, open banking APIs, cloud services, fintech partners, fraud systems, and customer data platforms.

That expansion creates opportunity. It also creates security complexity.

In 2026, the challenge is not whether banks should perform threat modeling. Most security leaders already recognize its value. The real challenge is how to scale threat modeling without slowing delivery, overwhelming engineering teams, or creating documentation that fails to influence real risk decisions.

For many institutions, manual threat modeling has reached its ceiling. Workshops are helpful, but they are often inconsistent. Diagrams become outdated. Findings are difficult to compare across applications. High-risk systems get attention, while smaller but business-critical applications may go unreviewed for too long.

A scalable program requires a different operating model: one that is risk-based, repeatable, measurable, and aligned to banking application security and finance and banking compliance needs.

Why Manual Threat Modeling Breaks Down in Banking Environments

Manual threat modeling challenges usually appear slowly, then all at once.

At first, security teams can manage a few workshops for major applications. Over time, the application portfolio grows. Business units launch new digital products. Engineering teams move faster. Vendors introduce new integrations. Cloud architectures change. APIs multiply. Soon, the threat modeling process becomes dependent on a small number of security experts who cannot keep pace with the business.

Common issues include:

- Inconsistent quality across teams and applications

- Limited visibility into shared risks across the portfolio

- Threat models that are completed once and rarely revisited

- Overreliance on static diagrams and manual notes

- Difficulty mapping threats to control gaps, compliance obligations, and remediation ownership

- Lack of prioritization between theoretical threats and business-impacting attack paths

For banking applications, this gap matters. A missed threat is not just a technical oversight. It can create exposure across customer trust, fraud prevention, transaction integrity, privacy, operational resilience, and regulatory expectations.

The 2026 Model: Risk-Based Threat Modeling at Scale

Scaling threat modeling does not mean turning every engineer into a security architect. It means building a system where risk context, application architecture, attacker behavior, and compliance needs work together.

A mature program should help teams answer five questions:

- What are we protecting?

- Who would target it, and why?

- How could the system be abused?

- Which controls reduce the most meaningful risk?

- How do we prove progress over time?

This is where advanced threat modeling for mid-sized banks becomes valuable. The goal is not to produce more documents. The goal is to create better security decisions earlier in the software lifecycle.

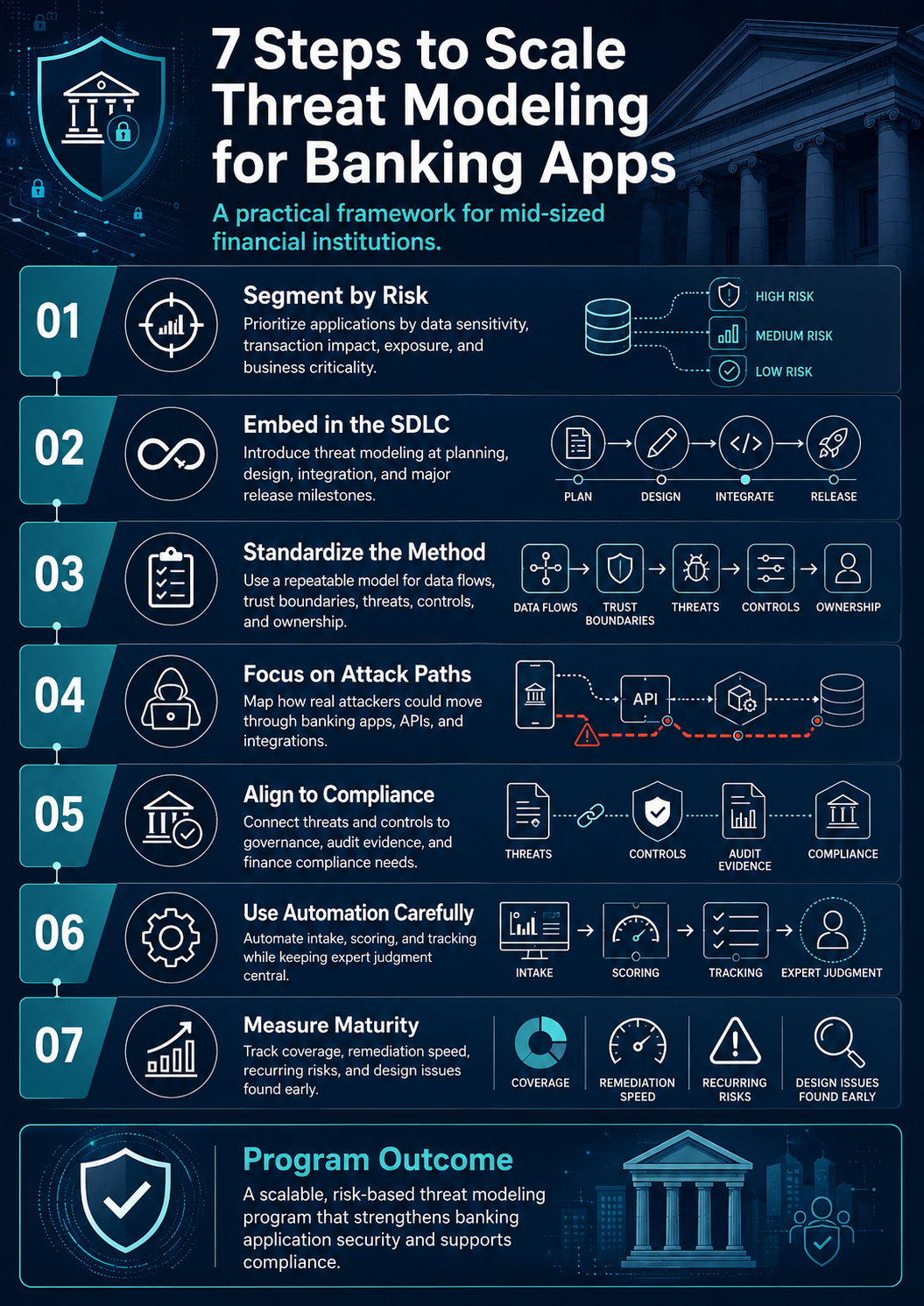

Step 1: Segment Applications by Business and Security Criticality

Start by classifying applications based on risk, not convenience.

A public-facing loan application portal, a payment processing workflow, and an internal reporting dashboard do not require the same level of threat modeling depth. Treating them equally wastes time and creates security fatigue.

A practical segmentation model should consider:

- Customer data sensitivity

- Transaction or payment impact

- Authentication and authorization complexity

- Internet exposure

- API connectivity

- Third-party dependencies

- Fraud or abuse potential

- Regulatory and audit relevance

- Business criticality and recovery expectations

This creates a tiered model. High-risk applications receive deeper analysis, more frequent review, and stronger validation. Lower-risk applications still receive baseline coverage, but with lighter-weight methods.

This is the foundation for scalable threat modeling services for financial institutions: focus the deepest expertise where compromise would have the greatest impact.

Step 2: Build Threat Modeling Into the Software Development Lifecycle

Threat modeling should not live as a one-time meeting before launch. By then, architecture decisions are already made, delivery pressure is high, and security recommendations are harder to implement.

Instead, embed threat modeling into key delivery moments:

- Product planning for new digital banking capabilities

- Architecture design for new systems or major changes

- API design and integration planning

- Cloud migration or infrastructure redesign

- Vendor onboarding and third-party connectivity

- Pre-release security review for high-risk changes

- Post-incident lessons learned

For mid-sized financial institutions, the most effective approach is often a hybrid model. Security teams provide standards, facilitation, and oversight. Engineering teams own repeatable inputs such as data flows, trust boundaries, and abuse cases. Leadership receives portfolio-level visibility into risk trends and remediation progress.

Step 3: Standardize the Method Without Making It Rigid

A scalable program needs consistency. It should not depend on who runs the workshop or which team owns the application.

Standardize the core elements:

- Application overview

- Data classification

- Trust boundaries

- User roles and privilege levels

- External integrations

- Authentication and session flows

- API exposure

- Threat scenarios

- Existing controls

- Control gaps

- Risk ratings

- Remediation owners

- Validation evidence

However, standardization should not become bureaucracy. Banking environments require flexibility. A mobile banking application, a fintech API integration, and an internal treasury platform will have different threat patterns.

The method should be consistent enough to compare risk across the portfolio, but adaptable enough to reflect real architecture and business context.

Step 4: Move From Threat Lists to Attack Paths

One of the most common weaknesses in manual threat modeling is the creation of generic threat lists. These lists may be technically accurate, but they often fail to show how an attacker would move through a system.

A stronger model focuses on attack paths.

For example, instead of listing “authorization failure” as a general issue, map how a user could manipulate an API request to access another customer’s account data. Instead of listing “third-party integration risk,” examine how a compromised vendor credential could affect transaction workflows or sensitive records.

Attack-path thinking helps teams connect application design to business impact. It also makes remediation easier to prioritize because the risk is tied to a plausible outcome.

Step 5: Align Threat Modeling With Compliance Evidence

Finance and banking compliance teams do not need more disconnected security artifacts. They need evidence that security controls are intentional, risk-informed, and maintained over time.

Threat modeling can support compliance by documenting:

- Why specific controls were selected

- Which risks were accepted, mitigated, or transferred

- How security requirements were defined before implementation

- Where third-party integrations introduce risk

- How remediation decisions were prioritized

- What validation activities confirmed control effectiveness

This creates a bridge between application security and governance. Instead of treating compliance as a separate reporting exercise, threat modeling becomes part of the institution’s defensible security program.

Step 6: Use Automation Carefully and Keep Expert Judgment Central

Automation can help scale threat modeling, but it should not replace security thinking.

Automated workflows can support:

- Application intake

- Architecture questionnaires

- Reusable threat libraries

- Control mapping

- Risk scoring

- Ticket creation

- Reporting dashboards

- Portfolio trend analysis

The risk is assuming that automation alone understands the business context of banking systems. It does not. A tool may identify a potential weakness, but experienced security professionals are still needed to interpret exploitability, customer impact, fraud potential, operational consequences, and regulatory relevance.

This is especially important for institutions evaluating threat modeling service providers. The right partner should bring more than templates or tooling. They should understand how application architecture, adversary behavior, governance, and business risk intersect.

Step 7: Measure Maturity, Not Activity

A scalable threat modeling program should be measured by outcomes, not the number of workshops completed.

Useful metrics include:

- Percentage of critical applications with current threat models

- Number of high-risk design issues identified before release

- Time to remediate threat modeling findings

- Recurring threat patterns across application teams

- Reduction in late-stage security defects

- Coverage of third-party and API-connected systems

- Alignment between threat model findings and security testing results

These metrics help security leaders show progress in terms executives understand: reduced exposure, better prioritization, faster remediation, and stronger governance.

PASTA for API Testing Free eBook

APIs are the backbone of modern applications, but they also increase the attack surface. Securing them requires more than basic testing. It requires a risk-based approach that connects business objectives, threat modeling, vulnerability analysis, and realistic attack simulation.

What Good Looks Like for Mid-Sized Banks

A mature threat modeling program for banking applications should feel practical, not performative.

Engineering teams should understand what is expected of them. Security teams should spend less time chasing diagrams and more time analyzing meaningful risk. Compliance stakeholders should be able to trace security decisions back to documented threats and controls. Executives should see which application risks matter most and where investment is needed.

Most importantly, threat modeling should help the institution make better decisions before weaknesses become production issues.

How VerSprite Approaches Scalable Threat Modeling

VerSprite’s approach to application security has always been rooted in adversary perspective, business context, and risk-based prioritization. For financial institutions, that matters.

Banking applications are not just software systems. They are trust systems. They move money, protect identity, enable access, and connect customers to critical financial services. Securing them requires more than vulnerability detection. It requires understanding how design decisions can create exploitable paths to business impact.

For mid-sized banks and financial institutions, VerSprite helps transform threat modeling from a manual exercise into a scalable application security capability. That means combining structured methodology, security risk assessment for fintech and banking environments, application architecture review, control validation, and actionable remediation guidance.

The result is a program that supports secure delivery, stronger governance, and better alignment between security leadership, application teams, and compliance stakeholders.

Final Takeaway

In 2026, threat modeling should no longer be treated as a specialized workshop reserved for only the largest banking applications. It should be a repeatable, risk-based capability built into the way financial institutions design, build, and maintain software.

For mid-sized institutions, the opportunity is clear: move beyond manual threat modeling challenges and establish a scalable program that reflects how modern banking applications actually operate.

The institutions that succeed will be the ones that make threat modeling practical, measurable, and connected to business risk.

Learn more: Financial & Banking Security Solutions

FAQ: Scaling Threat Modeling for Banking Applications

What is threat modeling for banking applications?

Threat modeling for banking applications is a structured security process used to identify how attackers could abuse an application, API, workflow, or integration before those weaknesses become production risks. For financial institutions, it helps connect application design decisions to business risks such as fraud, unauthorized access, data exposure, transaction manipulation, and compliance gaps.

Why do mid-sized financial institutions need scalable threat modeling?

Mid-sized financial institutions often manage complex application portfolios with limited security resources. Scalable threat modeling helps teams prioritize the highest-risk systems, reduce manual review bottlenecks, and build repeatable security practices across banking applications, APIs, cloud environments, and fintech integrations.

What are the biggest manual threat modeling challenges?

Common manual threat modeling challenges include inconsistent documentation, outdated architecture diagrams, limited security team capacity, difficulty comparing risks across applications, and findings that are not clearly tied to remediation ownership. These issues make it harder for security leaders to manage application risk at scale.

How does threat modeling support finance and banking compliance?

Threat modeling supports finance and banking compliance by documenting security risks, control decisions, remediation priorities, and evidence of secure design review. This helps institutions show that application security decisions are risk-based, repeatable, and aligned with governance expectations.

When should a banking application be threat modeled?

A banking application should be threat modeled during early design, before major releases, when APIs or third-party integrations are introduced, during cloud migration, after significant architecture changes, and after security incidents that reveal design-level weaknesses.

What should financial institutions look for in threat modeling service providers?

Financial institutions should look for threat modeling service providers that understand banking application security, adversary behavior, secure software design, compliance expectations, and business risk. The right provider should deliver actionable findings, not just generic threat lists or template-based documentation.

Share

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /

- /